This article answers common questions our clients often ask at the outset of a personal injury case. We hope you find it helpful.

1. What if I Can’t Pay My Medical Bills?

Depending on the nature of your case, your medical bills may be covered by one or more of the following:

- Your health insurance.

- Health insurance obtained by your spouse (or your parents, if you are underage) for your benefit.

- If you were driving your car and involved in a collision, medical payments insurance coverage from your auto policy.

- Medical payments insurance coverage from the person you were riding with, if you were a passenger in an automobile that has auto insurance coverage.

- Workers’ compensation insurance, if you were injured on the job and the injury occurred as a result of your employment.

- The liability insurance coverage for the person, persons or company who caused your injuries. This coverage likely will be paid at the time of settlement, rather than when you incur your medical bills.

If you have no insurance coverage, save your medical bills so that they can be paid at a later date, when and if your case settles. If you are unable to pay your bills as they are incurred, many doctors, hospitals, and other medical facilities will wait to receive payment until your personal injury case is resolved by way of a settlement or a verdict in court.

It is important to let your medical providers know, early in the process, if you have no insurance or financial means to pay your medical bills as they are incurred. Many doctors and medical facilities will require that you sign a form (usually called a “subrogation” or “lien” form), which allows your attorney to withhold enough money from any settlement or verdict to pay your medical bills directly from the insurance settlement proceeds.

2. Why Won’t the Insurance Company for the Person or Entity Who Caused My Injuries Automatically Pay My Medical Bills as They Are Incurred?

Most insurance companies for the party who caused another person to be injured will not automatically pay medical bills as they are incurred for two primary reasons: First, the insurance company does not want to spend a substantial amount of money for medical bills up front, only to be faced with an unreasonable or excessive demand at the time of final set- tlement.

Put another way, the insurance company does not want to expend a substantial sum of money on medical bills and then be faced with the possibility of defending a lawsuit. Second, most insurance companies want to conclude or settle the claim with one sum of money. Therefore, most liability insurance companies will wait for a settlement demand from the injured party or his or her attorney and then try to conclude the case all at once with one payment.

3. Do I Really Need a Personal Injury Lawyer?

You may choose to handle your personal injury claim on your own, but having an experienced personal injury lawyer on your side will improve your chances of obtaining a favorable outcome. An attorney is trained in the law, and under- stands the rules of evidence and procedure. Perhaps more importantly, an attorney can rely on the wisdom gained from hard-earned experience in dealing with claims adjusters and defense attorneys. Here are just some of the ways a personal injury lawyer can help you resolve your claim:

- Conduct a thorough investigation into the facts surrounding the incident, including:

- Interview witnesses and take statements.

- Visit the scene of the incident to take photographs and notes, and make a diagram.

- Obtain the police report, if one exists.

- Obtain and review your medical records and any statements made by you or witnesses.

- Analyze the facts of your case, in light of the law in your jurisdiction, to answer the most basic question: Do you have a case?

- Prepare a demand letter in a format that encourages the adjuster to negotiate a prompt, fair and reasonable settlement.

- Quickly recognize and deal with adjuster negotiation strategies, tactics and tricks.

- Guide your case through the litigation process, including:

- Timely file a lawsuit that names all the potentially responsible parties as defendants and raises all viable legal claims.

- Serve written discovery on the defendants and take depositions.

- Help you prepare for your deposition and attend the deposition with you to protect your rights.

- Retain experts.

- Present your case to a jury at trial.

You may be able to do some or all of these tasks on your own, but a personal injury attorney will do them more efficiently and effectively.

4. What if I Can’t Afford a Lawyer?

Most personal injury cases are handled on a “contingency” basis, which means that you do not have to pay attorney’s fees unless you receive a favorable settlement or verdict. In other words, your attorney’s fee is “contingent upon” a settlement or successful court award. Your lawyer’s fee will be calculated as a percentage of your recovery.

Note: It is important to distinguish between “fees” and “costs.” Your attorney’s fee is based upon his or her work, time, effort and expertise, as well as certain fixed expenses, e.g., secretarial time and rent. The costs (i.e., other out-of-pocket expenses) associated with representing you are your responsibility. These costs cover things like the cost of obtaining medical reports; photocopies; experts’ fees; and preparing exhibits. Your attorney may ask you to pay these costs as they are incurred.

5. How Long Will It Take To Resolve My Case?

This question is impossible to answer with certainty because the facts of each case are unique. In general, though, it will take several months to settle a personal injury claim. If you want to settle your case on your own, without the assistance of a lawyer, it may take longer. If your case does not settle, it may take several years to resolve through the court system. This is because:

- Your case will not be ripe for settlement until all the facts are known and the full nature and extent of your injuries is established. Your lawyer must have all of the medical reports and bills from all of your doctors, and must have thoroughly investigated all of the facts. When a liability case is settled, it is settled for one lump sum, and the settlement is final. Any increased expenses – additional lost wages or increased medical expenses as a result of a change in your physical condition – cannot be the subject of future claims once the case has been settled. For this reason, your lawyer will wait until he has all the facts before attempting to settle your claim.

- In general, insurance companies are in no rush to settle smaller personal injury claims. Adjusters will engage in a host of negotiating “tactics” designed to delay settlement of the claim in an effort to put pressure on you to settle for less.

- The litigation process – particularly the discovery phase of the litigation – takes time.

- Most court dockets are overcrowded with cases, resulting in unavoidable delays.

6. What Is the Potential Value of My Case?

Early in a personal injury case, this is the most difficult question to answer because there are so many variables at play: the full nature and extent of your injuries is not yet known; your medical treatment is ongoing; and you may be uncertain as to when you can return to work. Accordingly, we can’t put a specific dollar value on your case at this time. We can, though, explain how you might be compensated, depending on the facts of your case:

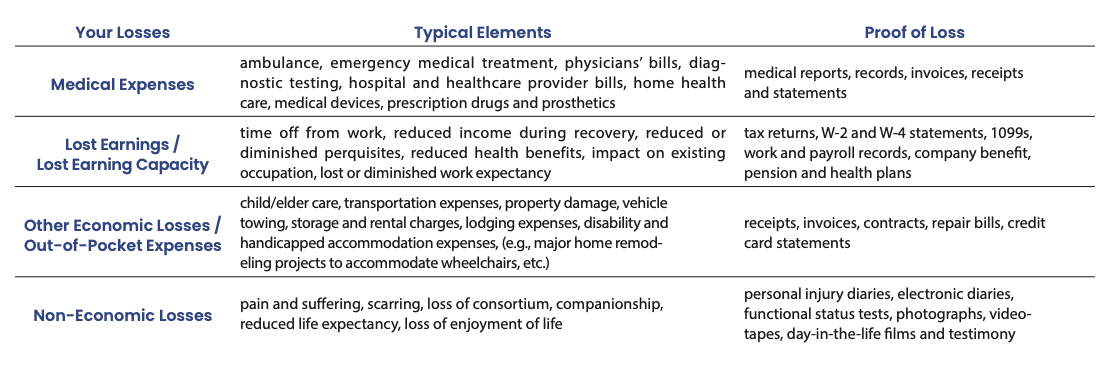

In legal terms, the value of your case is measured in terms of “damages.” To put it another way, when you are injured by another person’s negligence (unreasonable carelessness), you may be entitled to a sum of money to compensate you for the harm you have suffered; this sum of money is called “damages” or “compensatory damages.” The goal of compensatory damages is to replace what the injured party has lost and make him or her whole again (inasmuch as money can do that). There are two components to compensatory damages: economic losses and non-economic losses.

Economic Losses

Economic losses are those losses that are quantifiable and verifiable. Medical expenses are a prime example. As part of compensatory damages, you are entitled to reimbursement for all reasonable and necessary medical expenses, including past and future medical expenses. Your medical bills will serve as proof of those expenses. Other economic losses for which you might obtain compensation include:

- Lost wages and benefits;

- Loss of future earning capacity;

- Miscellaneous expenses (e.g., childcare, transportation, medical devices or appliances, etc.); and

- Property damage.

Non-Economic Losses

Non-economic losses are those that are not easily quantifiable. This category of damages includes compensation for emotional distress; pain and suffering; permanent injuries, scarring and disfigurement; and loss of enjoyment of life. The value of your non-economic losses is subjective; no exact formula exists for making this calculation.

The chart below summarizes the key components of damages and illustrates possible means of proving each component.

Get a Free Case Consultation

Before you negotiate or sign anything, learn your rights and how to protect yourself and your family. A personal injury lawyer can talk to you about your legal options, how to avoid common mistakes, and how to maximize your claim.

Contact McKay Law now to discuss your case at (903) INJURED / (903) 465-8733 or (903) ABOGADA / (903) 226-4232. The consultation is free, and there is no obligation. NO FEES UNLESS WE WIN!